Concept of Lifecycle of Bond–Accounting Events for Oracle Financial Accounting Hub

Accounting aspects of financial instruments as per IFRS 9, particularly bonds, essential in planning and implementing of Oracle Accounting Hub Cloud Service (AHCS).

Let us first understand bonds. These are commonly used sources of finance by companies wherein they borrow funds from investors by issuing securities. Bonds are clearly different from equity (shares) since the whole idea of bond is based on loans. One might ask: how can security be categorised as a bond? The answer is simple—issuer of bond will have an obligation of contractual cash outflows of interest and principal.

Before moving on to the accounting aspects, let us understand some commonly used terms:

- Issuer – Refers to corporate, bank, financial institution borrowing funds by issuing bonds.

- Investor – One who invests in bond and is entitled to receipt of interest and principal payments.

- Face Value – The value of bond which will be repaid to investor at maturity. Also, the interest payable is calculated on this value.

- Coupon Rate – The rate of interest payable on bonds.

- Maturity Date – The date on which issuer pays the face value of bond to investor.

- Issue Price – The price at which issuer originally sells the bond.

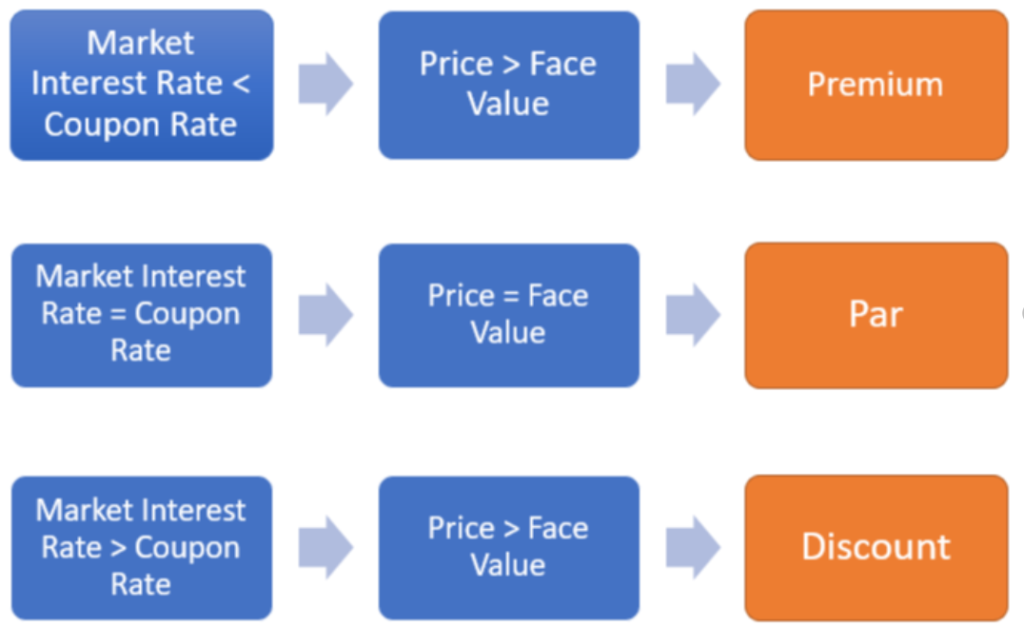

In a practical scenario, there is a time gap in the announcement of issue at stated coupon rates and actual issue of bonds. It is obvious that the interest rates on securities in the market may rise or fall by the time of issue, it is for this reason that the issue price of bond may not be same as the face value.

Therefore, based on movement of interest rates and resultant price, the bonds can be of following types

Let us consider a scenario where

- The face value of 1000 bonds is $100 each. The face value of the issue is $100,000.

- The coupon rate is 8%, payable annually.

- The life of bond is 4 years.

- At the time of issue, the market rate of interest drops to 7%.

Considering a career in cloud?

Now, the issuer must consider the following accounting events for the entire lifecycle of the bond

- Receipt of funds in exchange of bonds

- Payment of interest on bonds

- Repayment of face value at maturity

Each of the events is discussed below:

1. Receipt of Funds in exchange of bonds – The issuer receives cash from investors and in return, creates a liability to return the face value to investors after 4 years. However, since the issue price is certainly higher than the face value, the liability should be booked at fair value.

Following Journal would have an effect

Cash A/c Dr (issue price) xxxx

To Bond Payable (Issue Price) xxxx

2. Payment of interest on bonds – The actual interest as per contractual obligation is $8,000 ($100,000 * 8%). However, the interest expense should be booked at the market rate and should be calculated on the issue price.

Following Journal would have an effect

Interest expense A/c Dr (issue price * 7%) xxxx

Bond payable A/c Dr (shortfall of interest expense) xxxx

To Cash $8,000

The above Journal would be passed at the end of the year for 4 years. ‘Shortfall of interest expense’ is the difference of $8000 and Interest expense, which in fact, is the additional price of the bond that is reduced from the bond liability. The liability thus gets reduced with a portion of the additional price.

Similarly, a portion of the additional price is reduced from the bond liability every year and at the end of 4th year, this liability gets reduced to $100,000, which is the promised face value.

3. Repayment of face value at maturity – At the end of 4th year, the bond liability is reduced to $100,000.

Following Journal would have an effect

Bond Liability A/c Dr $100,000

To Cash $100,000

The detailed calculation is available in this excel sheet.

Above mentioned natural accounts would get affected in the accounting of any other type of bond. Here are some useful links to get a detailed understanding of bonds, its types, characteristics, and accounting aspects thereof.

- A glimpse of AHCS – https://www.oracle.com/a/ocom/docs/applications/erp/oracle-accounting-hub-cloud-ds.pdf

- Basics of Bond – https://www.investopedia.com/terms/b/bond.asp

- Accounting Scenarios – https://opentextbc.ca/principlesofaccountingv1openstax/chapter/prepare-journal-entries-to-reflect-the-life-cycle-of-bonds/

Hello my friend! I wish to say that this post is amazing, great written and include approximately all vital infos. I would like to see extra posts like this .